The Balanced Scorecard (BSC) process can align operational activities with an organisation’s vision, improve internal and external communications, and monitor organisation performance against strategic goals. It is best considered a value-based strategic planning and management tool that can assist extension professionals and their client’s best consider what areas a business needs assistance with.

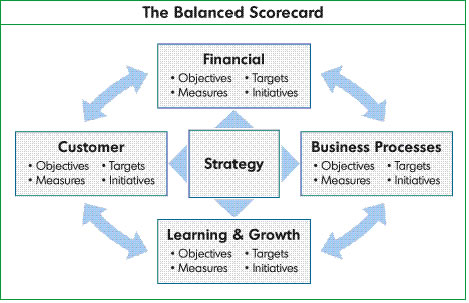

The Balanced Scorecard (BSC) provides a “balanced” assessment of an organisation’s/business performance by linking financial with non-financial performance indicators across four distinct perspectives:

- Learning and growth

- Internal business process

- The customer, and

- The financial.

The Four Key Perspectives Explained

The Balanced Scorecard paradigm views a strong financial performance as a result of the successful implementation of strategic initiatives across the four key business perspectives, rather than positioning financial activities as the driver of success (Freier and Protil, 2009).

- The Learning & Growth Perspective – learning and growth constitutes an essential foundation for success of any knowledge intensive organization. Learning and growth performance includes the consideration of:

- Employee training, mentors and tutors within the organisation

- Ease of communication between staff to enable a supportive learning environment

- Workplace cultural attitudes towards both individual and organisational self-improvement, and

- ICTs (Information and Communication Technologies).

In the current climate of rapid technological change, it is becoming necessary for knowledge workers to be in a continuous learning mode.

- The Business Process Perspective – refers to internal business processes. Metrics based on this perspective allow the managers to know how well their business is running, and whether its products and services conform to end-user requirements. These metrics need to be carefully designed by those who know these processes most intimately – an organisation’s mission is not something that can be developed by outside consultants.

- The Customer Perspective – recent management philosophy has shown an increasing realisation of the importance of having an end-user focus and a business goal of achieving “customer” satisfaction. From this perspective, poor customer service is a leading indicator of future decline, even though the current financial picture may look good. In developing metrics for satisfaction, customers should be analysed in terms of customer type and the kinds of processes that are used to provide a product or service to those customer groups.

- The Financial Perspective – Kaplan and Norton do not disregard the traditional need for financial data. Timely and accurate funding data will always be a priority, and managers will do whatever necessary to provide it. However current emphasis on financials leads to the “unbalanced” situation with regard to other perspectives. There is perhaps a need to include a risk assessment and cost-benefit data.

The Balanced Scorecard links these perspectives with one another, together with revenue growth and the overall strategy of the organisation, to create a “causal-loop-learning” model. Generally speaking, improving performance in the objectives found in the Learning & Growth perspective enables the organisation to improve its internal processes, which in turn enables it to create desirable results in the Customer and Financial perspectives (Balanced Scorecard Institute, 1998-2016).

Figure 1: A representation of the key elements of the Balanced Scorecard

Putting a balanced scorecard into practise requires clarifying the vision and strategy, communicating and linking, planning and target setting and strategic feedback and learning. The BSC is best considered as a value-based planning and management tool.

History

The Balanced Scorecard was developed by Dr. Robert Kaplan (Harvard Business School) and David Norton in the 1990s to introduce and link non-financial indicators with financial indicators to provide a more “balanced” overview of an organisation’s business performance. Kaplan and Norton argued that the traditional financial approach was insufficient in linking long-term and short-term actions with the non-financial factors, which impact on the complex performance of any organisation/business.

Content source and further Information

Balanced Scorecard Institute (1998-2016) Balanced Scorecard Basics, http://balancedscorecard.org/Resources/About-the-Balanced-Scorecard

Freier, A. E. and Protil, R.M., (2009), Developing methods for strategic evaluation in agricultural research and production, No 58016, 113th Seminar, September 3-6, 2009, Chania, Crete, Greece, European Association of Agricultural Economists. http://ageconsearch.umn.edu/bitstream/58016/2/Freier.pdf Kaplan, R. and Norton, D. (1996) ‘Balanced Scorecard: Translating Strategy into Action’, Harvard School Press.